© The Indian Express Pvt Ltd

Premium

The Bharti Airtel story: From survival to revival in India’s telecom battlefield

Bharti Airtel, once on the brink of being overshadowed by the aggressive pricing war in India’s telecom sector, has staged a remarkable comeback. From facing intense competition during the Jio revolution to making strategic moves in 5G deployment, Airtel’s resilience has positioned it as a formidable player once again. A look at how the company regained its ground in the cutthroat telecom market.

Written by Sonia Boolchandani

April 4, 2025 12:22 IST

April 4, 2025 12:22 IST

Operators like Airtel focused on expanding their networks to every corner of the country, building towers in remote villages and small towns where landlines had never reached. (Reuters)

Operators like Airtel focused on expanding their networks to every corner of the country, building towers in remote villages and small towns where landlines had never reached. (Reuters)Remember 2016? The year demonetisation happened, Pokémon GO took over the world, and Indians were still paying around Rs 250 for a single GB of mobile data. Then came September, and everything we knew about telecom in India changed forever.

Reliance Jio stormed into the market with an offer that seemed like financial suicide: free calls and data at prices that made other operators gasp. Overnight, the rules of India’s telecom game were rewritten. Data went from being a luxury to a commodity. Voice calls, once the industry’s cash cow, became practically worthless.

The industry’s lifeblood metric — Average Revenue Per User (ARPU) — crashed from Rs 120 to Rs 71 within four years. To put this in perspective, imagine running a restaurant where your average bill value drops by nearly 40% but your rent, salaries, and ingredient costs remain unchanged. That’s essentially what happened to telecom operators.

Many couldn’t survive the onslaught. Remember Aircel? Tata Docomo? Telenor? They’re all gone now. Even giants like Vodafone and Idea were forced into a marriage of necessity. From a vibrant market with over a dozen players, India’s telecom sector condensed into a three-horse race: Jio, Airtel, and the merged Vodafone Idea (Vi).

Yet amidst this carnage, Bharti Airtel not only survived but managed to reinvent itself. How did a company facing an existential threat transform into a digital powerhouse with the industry’s highest ARPU and healthiest balance sheet? That’s the story we’re unpacking today.

The 4 acts of India’s telecom drama

Act 1: The dawn of mobile revolution (2000-2010)

The millennium began with a groundbreaking policy change. The National Telecom Policy of 1999 transformed India’s telecom landscape by allowing operators to expand nationwide with limited upfront investments. This was revolutionary — telecom companies could now build networks across India without breaking the bank on licences and permits.

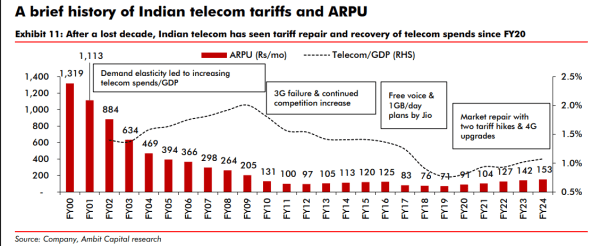

What followed defied conventional business wisdom. Despite average revenue per user (ARPU) plummeting from a staggering Rs 1,319 per month to just Rs 131 (a jaw-dropping 90% decline), the industry’s revenue grew at a healthy 17% annual rate between 2002 and 2010. Telecom’s contribution to India’s GDP increased from 1.4% to 1.8%.

Story continues below this ad

How could falling prices lead to rising revenues? The answer is simple — explosive growth in subscribers. As mobile services became more affordable, millions of Indians embraced cellular technology. The mobile phone transformed from a luxury gadget for the elite to an essential tool for the masses. Operators like Airtel focused on expanding their networks to every corner of the country, building towers in remote villages and small towns where landlines had never reached.

During this period, Airtel emerged as the market leader, building a reputation for network quality and customer service. The company’s iconic ‘Express Yourself’ campaign captured the imagination of a newly connected India. While prices fell, volumes surged, creating a virtuous cycle of growth.

Act 2: The era of cutthroat competition (2010-2015)

By 2010, India’s telecom success story had attracted too many players to a market that couldn’t sustain them all. New entrants like Telenor, MTS, Videocon, and Tata Teleservices (GSM) joined established players like Airtel, Vodafone, Idea, and Reliance Communications in a pitched battle for market share.

This period witnessed the introduction of per-second billing for voice calls. Remember those ads promising “only pay for what you use”? While consumers benefited from these micro-billing innovations, they squeezed operator margins further.

Story continues below this ad

Meanwhile, telecom companies collectively spent billions on 3G spectrum in 2010, hoping to usher in the mobile internet revolution. However, 3G largely failed in India due to a combination of regulatory constraints and technological limitations. Spectrum availability was restricted, and the smartphone ecosystem was still in its infancy. It was a classic case of right idea, wrong timing — companies spent big on licences but couldn’t monetise them effectively.

The result? Industry ARPU continued its downward slide from Rs 131 to Rs 120, and telecom’s contribution to GDP retreated from 1.8% to 1.4%. This phase clearly demonstrated that excessive competition was hurting everyone — consumers might have been getting cheaper services, but the industry was becoming financially unsustainable.

For Airtel, this meant focusing on operational efficiency while maintaining network quality. The company began expanding beyond traditional telecom services into areas like direct-to-home television and enterprise solutions, laying the groundwork for its future digital ecosystem.

Fig 1: A brief history of India’s telecom tariffs and ARPU

Fig 1: A brief history of India’s telecom tariffs and ARPU

Act 3: The Jio tsunami and industry upheaval (2016-2019)

Then came the tsunami that permanently altered India’s telecom landscape: Reliance Jio’s entry in September 2016.

Story continues below this ad

Jio’s launch strategy was unprecedented globally. The company offered a six-month free trial period, allowing customers to use unlimited voice and data services without paying a single rupee. When Jio finally started charging in April 2017, its plans were still priced about 25% below the industry average. But the real disruptors were the inclusions:

Free unlimited voice calls when other operators were charging over Rs 0.3 per minute

Daily data allowances of 1GB+ when incumbents were offering monthly data caps of 1GB

Free access to Jio’s content ecosystem including music, movies, and TV shows

Story continues below this ad

What made this possible? By 2016, Jio had already invested a staggering US$30 billion, approximately 25% more than market leader Airtel’s cumulative investments at the time. This massive capital infusion from parent company Reliance Industries allowed Jio to build a 4G-only network with enormous data capacity that competitors couldn’t match with their predominantly 2G and 3G networks.

Regulatory factors also played a role. Unlike in developed markets where predatory pricing is strictly controlled, Indian regulators allowed Jio’s aggressive strategy to proceed without significant intervention.

The impact was devastating for the industry. Almost overnight, voice calls — previously the main revenue source for telecom operators — became free. Data prices crashed by over 90%. Industry ARPU plummeted to just Rs 71 in FY19, down from Rs 120 in FY15. Telecom spending as a percentage of GDP collapsed to 0.8%, among the lowest globally.

The sector witnessed rapid consolidation as weaker players exited or merged:

Airtel acquired Videocon, Telenor, Aircel, Tikona, and Tata Teleservices

Vodafone and Idea merged to form Vodafone Idea

Story continues below this ad

Smaller players like Aircel and Reliance Communications filed for bankruptcy

What began as a market with over 10 operators quickly transformed into a three-player market (plus state-owned BSNL/MTNL).

For Airtel, this period was about survival and adaptation. The company doubled down on premium customers, focused on quality of service over pricing, and accelerated its digital transformation. While many competitors faltered, Airtel managed to weather the storm despite taking significant financial hits.

Act 4: The gradual recovery and focus on sustainability (2019-Present)

The turning point came in October 2019 after the Supreme Court’s verdict in the long-standing Adjusted Gross Revenue (AGR) case. The court ruled that telecom companies had to pay dues based on a broader definition of revenue, resulting in liabilities of approximately Rs 92,000 crore.

Story continues below this ad

Faced with this financial pressure and unsustainable tariffs, telecom operators finally hiked rates by 30-50% in December 2019. This marked the beginning of tariff repair after years of decline.

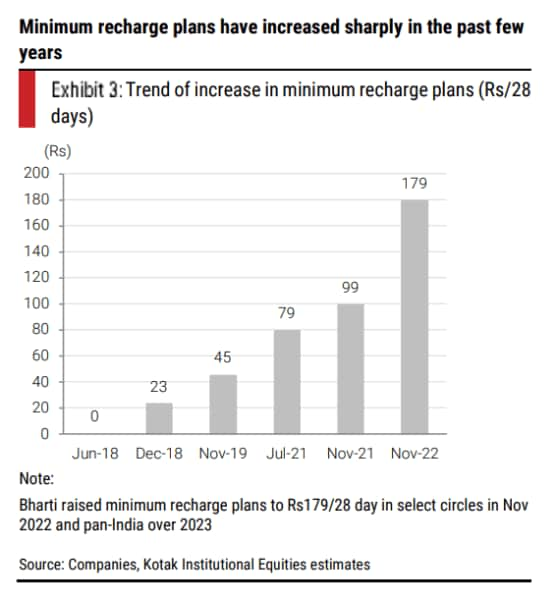

A second tariff hike of 20% followed in December 2021, driven by continued financial stress. Additionally, both Airtel and Vi gradually eliminated their minimum recharge plans in favour of unlimited voice plans, further improving ARPU.

Government reforms in September 2021 also provided relief, introducing a four-year moratorium on spectrum and AGR dues, reducing bank guarantee requirements, and allowing 100% foreign direct investment through the automatic route.

Despite these positive steps, telecom spending as a percentage of GDP remains at just 1.07% in FY24 — better than the low of 0.77% in FY19, but still below the pre-Jio level of 1.36% and far from the 2% of FY09.

Story continues below this ad

Several factors have made operators cautious about aggressive tariff hikes:

- The COVID pandemic affected affordability for marginal telecom users

- Smartphone prices increased by 56% between 2019 and 2023 due to chip shortages

- Consumer spending on smartphones jumped 51% during this period

For Airtel, this period has been about strategic repositioning. The company has focused on:

- Premiumisation of its customer base

- Expanding digital services beyond core telecom

- Building a converged ecosystem through Airtel Black

- Accelerating home broadband and enterprise business growth

- Rolling out 5G networks nationwide

The most recent tariff hike in July 2024 further improved Airtel’s financial position, with more expected to follow as the focus shifts from market share battles to ensuring adequate returns on investments.

Airtel today: Financial transformation and strategic priorities

With Vi’s recent fundraising providing some breathing room for the struggling operator, the dynamics are changing. Airtel and Jio can no longer count on easy subscriber gains from Vi, and their focus is likely shifting from simply grabbing market share to generating adequate returns through more frequent tariff hikes.

Airtel has consistently maintained that the industry needs to reach Rs 300/month ARPU to generate adequate returns on investments. The company has been leading the premiumisation trend, with its ARPU reaching Rs 245/month in the latest quarter — significantly higher than Jio’s Rs 203/month and Vi’s Rs 163/month.

This shift in strategy coincides with Reliance Jio also facing pressure to improve returns on its massive 5G investments. With a potential Jio Platforms IPO on the horizon in 2025, Jio is likely to be more willing to participate in industry-wide efforts to raise tariffs.

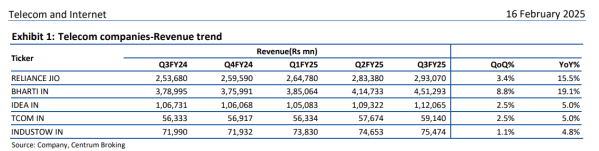

Fig 2: Telecom companies revenue trend

Fig 2: Telecom companies revenue trend

The free cash flow revolution

Here’s where Airtel’s story gets particularly interesting. Driven by tariff increases in its India wireless segment, Airtel’s free cash flow generation has improved dramatically. For the first nine months of FY25 alone, the company generated Rs 292 billion in free cash flow, up from Rs 213 billion for the entire FY24.

Until now, Airtel’s main priority has been deleveraging. The company has prepaid approximately Rs 670 billion of spectrum debt since FY22, clearing all spectrum liabilities from the 2012, 2014, 2015, and 2016 auctions. This strategic decision has significantly reduced interest costs and strengthened the balance sheet.

With a complete flow-through of the July 2024 tariff hike, a likely additional tariff increase of around 15% expected next year, moderating capital expenditure, and the consolidation of Indus Towers, Airtel is projected to generate approximately Rs 570 billion in free cash flow by FY27. After accounting for regulatory dues payments, this still translates to about Rs 500 billion — a substantial sum that raises important questions about capital allocation.

The capital allocation conundrum

With high-cost debt largely repaid and leverage ratios in a comfortable zone, capital allocation has become the most important factor that will drive Airtel’s stock performance in the medium term. The company’s remaining debt of about Rs 944 billion to the government primarily consists of AGR dues (under moratorium until March 2026 at an 8% interest rate) and 2022 spectrum payments (at around 7.2% interest rate).

Given the relatively benign interest rates on these obligations and ongoing hopes for some relief on AGR dues, further prepayments seem unlikely. Airtel’s net debt excluding deferred payment liabilities and lease obligations stands at a modest Rs 392 billion, compared to an annualised EBITDAaL (EBITDA after leases) of Rs 1.04 trillion. At current cash generation rates, this could be largely repaid by FY27.

So what will Airtel do with its growing cash reserves? The company has several options and competing priorities:

1. Increasing dividend payouts

One pressing reason for Airtel to boost dividends is the situation at Bharti Telecom Limited (BTL), the holding company that owns 40.5% of Airtel. BTL, a joint venture between Bharti Enterprises and Singtel (51:49), has accumulated around Rs 380 billion in debt, largely to purchase Airtel shares.

The debt-to-equity ratio at BTL has spiked to 5.4x as of December 2024, raising concerns about its financial stability. Since dividends from Airtel are BTL’s only revenue source, Airtel’s FY25 dividend payout would need to increase to at least Rs 14 per share (up from Rs 8) for BTL to service its interest payments.

Moreover, BTL faces significant near-term financial pressures:

It needs to either repay or refinance approximately Rs 215 billion in dues between September 2025 and February 2026

It has to contribute about Rs 58 billion toward pending calls on rights issues

It might need to purchase additional Airtel shares if Singtel looks to equalise its direct stake with Bharti or if the promoters want to consolidate their holdings under BTL

Given these requirements, increasing dividend payouts is likely to become a top priority for Airtel in the coming years.

2. Strategic investments in Africa

Airtel has recently purchased a 4.45% stake in Airtel Africa for approximately Rs 23.6 billion. While some investors might prefer higher dividends or investments in Indian operations, this move could be strategically sound.

Airtel Africa has been delivering robust double-digit growth in constant currency for several years and operates in markets with significant untapped potential for both data and mobile money services. Despite strong growth prospects, Airtel Africa trades at a relatively low valuation of around 3.8 times FY27 estimated EBITDA.

Several near-term catalysts could unlock value:

A potential sharp tariff hike in Nigeria (Airtel Africa’s largest market)

The upcoming IPO of its Mobile Money business in July 2025

Continued growth in both the telecom and financial services segments

The investment might also be more financially savvy than it appears at first glance. Airtel will likely be able to recoup much of this investment through upcoming inflows from Indus Towers, making the net financial impact relatively small.

3. Strategic mergers and convergence

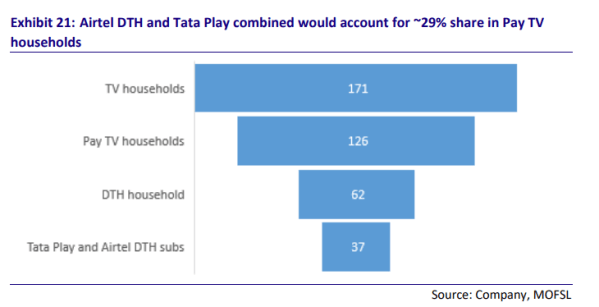

Airtel has confirmed it’s in discussions with the Tata Group to explore a potential merger between Airtel DTH and Tata Play. This comes at a challenging time for the DTH industry, which has seen subscribers decline from a peak of 72 million in March 2019 to about 60 million in September 2024.

Several structural headwinds face the DTH sector:

Competition from over-the-top (OTT) streaming platforms

Improving content availability on DD Free Dish (free-to-air service)

Regulatory caps on network capacity fees after NTO 2.0 implementation

Tata Play is India’s largest DTH provider with 19 million subscribers (approximately 32% market share), while Airtel DTH is second with 17.6 million subscribers (around 29% market share). While a merger might not create significant value for Airtel’s DTH operations on a standalone basis, it offers strategic benefits.

Fig 3: Airtel DTH and Tata Play

Fig 3: Airtel DTH and Tata Play

The real prize is access to Tata Play’s approximately 19 million high-paying households. Airtel could target these customers for its converged offerings under the Airtel Black brand, which bundles mobile, broadband, and DTH services. This aligns with Airtel’s strategy of focusing on premium customers and increasing revenue per household rather than just subscriber numbers.

The 5G revolution and beyond

Both Airtel and Reliance Jio have been aggressively expanding their 5G coverage across India. For Jio, approximately 170 million subscribers have migrated to 5G, compared to 120 million for Airtel. The companies have covered most districts in India and are gradually expanding to smaller towns and rural areas.

The 5G rollout has significantly increased the data capacity of telecom operators and now accounts for a substantial portion of total wireless data traffic. Initial monetisation efforts have begun, with unlimited 5G data available only on higher-value recharge plans.

However, the real potential of 5G goes beyond consumer mobile broadband:

- Fixed Wireless Access (FWA): Using 5G to provide home broadband in areas where fiber deployment is challenging or uneconomical

- Enterprise solutions: Private networks, IoT applications, and industry-specific use cases

- Edge computing: Leveraging 5G’s low latency for applications requiring real-time processing

- Network slicing: Creating virtual networks with different characteristics for specific applications

Airtel has been systematically building capabilities in all these areas, positioning itself not just as a connectivity provider but as a digital solutions partner for both consumers and businesses.

The competition landscape: A three-player market

While Airtel and Jio continue to strengthen their positions, Vi is making efforts to regain its footing.The company recently raised funds through a follow-on public offering (FPO), bringing the government’s stake to 23%.

Now, in a fresh move, the government has decided to convert another Rs 36,950 crore of the company’s dues into equity, nearly doubling its stake to 49%. This amount includes outstanding spectrum auction dues and deferred payments that would have otherwise become payable after the moratorium period, the telecom operator revealed in an exchange filing.

Meanwhile, Vi has announced plans to roll out 5G services by March-April 2025, starting with Mumbai, Delhi, Bangalore, and Patna. But despite the government’s backing, the company’s financial situation remains precarious. It still carries a net debt of Rs trillion, with a net debt-to-EBITDA ratio of 12 times based on FY24 earnings.

So, while the government’s intervention provides some relief, whether it’s enough to turn Vi’s fortunes around is still up in the air.

The competition dynamic has evolved significantly:

- Airtel has positioned itself as a premium provider focused on quality and digital services

- Jio continues to leverage its scale advantages while gradually moving upmarket

- Vodafone Idea is fighting for relevance, focusing on retaining existing subscribers while trying to upgrade its network

Fig 4: Minimum recharge plans

Fig 4: Minimum recharge plans

This three-player structure (plus state-owned BSNL/MTNL) has brought more rationality to the market after years of destructive competition.

The tower business: Indus Towers

A key part of Airtel’s story that often gets overlooked is its stake in Indus Towers, India’s largest tower company. Indus continues to see strong tower and co-location additions, driven by demand from 5G rollouts and Vi’s network expansion.

The long-standing issue of receivables from Vi is expected to see early resolution as cash flows improve for the troubled operator. This should further strengthen Indus Towers’ financial position and, by extension, benefit Airtel as a major shareholder.

The road ahead: Growth projections and strategic priorities

Looking forward, Airtel is projected to achieve a compound annual growth rate of approximately 15% in consolidated revenue and 19% in EBITDA between FY24 and FY27. This growth will be driven by:

More frequent tariff hikes in the India wireless business, potentially leading to a 12.5% ARPU compound annual growth rate

Acceleration in home broadband services as fiber deployment expands

Robust double-digit growth in Africa across both telecom and mobile money services

Expansion of enterprise and digital businesses including data centres, cloud services, and cybersecurity

With capital expenditure intensity moderating after the initial phase of 5G rollouts, Airtel is likely to generate significant free cash flow — approximately Rs 1.3 trillion over FY25-27 — leading to further deleveraging and improved shareholder returns.

The company’s management has indicated that deleveraging, increasing shareholder returns through higher dividend payouts, and bolt-on acquisitions to boost capabilities in the Enterprise business remain the key priorities for capital deployment.

The bottom line: From survival to strategic growth

Airtel’s journey from the chaotic early days of Indian telecom to its current position of strength is a testament to its resilience and adaptability. Having survived the Jio onslaught and positioned itself as a premium service provider, the company now faces the challenge of balancing shareholder returns, strategic investments, and continued growth.

The focus has shifted from merely surviving to thriving, from market share battles to generating adequate returns on investments. With improving financials and a clear strategy, Airtel appears well-positioned to capitalise on India’s ongoing digital transformation.

For investors and industry observers alike, the key questions revolve around:

- How Airtel will allocate its growing cash reserves

- Whether it can maintain its premium positioning in an increasingly competitive market

- How successfully it can monetise 5G and expand its digital ecosystem

- The potential for further consolidation in adjacent industries like DTH

As India moves toward a more mature telecom market with fewer players but healthier economics, Airtel’s strategic choices will not only shape its own future but also influence the broader evolution of digital services in one of the world’s largest and most dynamic markets.

The story of Bharti Airtel is, in many ways, the story of modern India’s digital journey — from expensive, limited connectivity to affordable, ubiquitous access. The next chapter promises to be about creating value through digital services and solutions rather than just providing the pipes that connect India.

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Sonia Boolchandani is a financial content writer. She has contributed her expertise to prominent firms, including 5Paisa, Vested Finance, and Finology, where she has crafted content that simplifies complex financial concepts for diverse audiences.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

Advertisement

Live Blog

Top Stories

Advertisement

Must Read

Advertisement

Buzzing Now

Apr 10: Latest News

- 01

- 02

- 03

- 04

- 05

Advertisement